Key takeaways

- Digital platforms enable governments and aid organizations to disburse emergency funds directly to those affected, minimizing the delays and losses associated with physical cash distribution. In Bangladesh, for example, the World Food Programme partnered with the bKash digital wallet platform to deliver anticipatory aid transfers ahead of Cyclone Amphan in 2020—helping vulnerable households to access food and other goods during the floods.

- During the COVID-19 pandemic, digital payments emerged as a cornerstone of economic and business resilience, enabling firms and consumers to adapt rapidly to new constraints. A 2021 VEEI survey found that U.S. small businesses selling online prior to the pandemic were able to maintain and grow their customer base as consumer behavior shifted rapidly toward e-commerce.

- In the case of geopolitical crises, digital payments can provide stability for individuals and businesses navigating new uncertainties and upheaval. Since the Russia-Ukraine war began, Visa data show that the use of digital financial services has allowed displaced persons to access their savings, pay for goods and services, and financially support themselves and their families while adjusting to new homes.

Frequent and complex shocks

In recent years, countries around the world have witnessed an escalation in the frequency, scale, and complexity of shocks. The 2024 INFORM Severity Index, a tool that quantifies crisis severity, found that there has been a global increase in the risk of humanitarian crisis over the last decade due to increased exposure to natural hazards and conflict.¹ By 2050, the Index estimates that the number of countries classified with “high” or “very high” crisis risk will increase by 45 percent. Across every continent, shocks such as protracted geopolitical conflicts, extreme climate events, and public health emergencies are becoming increasingly common and having far-reaching effects.

Economic impacts are among the most significant consequences of these shocks within a country. Shocks have the capacity to destabilize national economies, disrupt supply chains, reduce investor confidence, and strain public resources, which can threaten a country’s economic resilience and ability to effectively respond and recover. Digital financial services (DFS) offer an innovative means for strengthening resilience during and after crises, enabling countries to maintain financial inclusion, facilitate rapid assistance, and support overall recovery. Additionally, digital financial services provide impacted individuals with a means to continue purchasing goods and services and affected merchants with a means to continue doing business. As shocks often disrupt traditional banking infrastructure, the ability to facilitate transactions through digital means has helped to ensure continuity in formal economic activities. This paper explores the pivotal role digital financial services play in enhancing a country’s economic resilience and facilitating recovery in the face of severe shocks.

Digital penetration improves aid response

Access to digital financial services can significantly influence how individuals, households, and businesses respond to and recover from shocks such as natural disasters. One of the biggest advantages of digital financial services is the speed and efficiency with which humanitarian aid can be delivered. Digital platforms enable governments and aid organizations to disburse emergency funds directly to those affected, minimizing the delays, bottlenecks, and losses that can be associated with physical cash distribution. Based on a survey by Visa and Devex of nearly 1,000 humanitarian aid professionals, transferring funds to digital wallets or financial accounts are seen as the most secure (58 percent) and transparent (60 percent) types of direct humanitarian aid.² Beyond immediate assistance, digital financial products such as savings accounts, insurance, and accessible credit can help people build resilience ahead of crises and facilitate swift recovery in their aftermath.

The level of penetration of digital financial services within a country before a natural disaster critically influences the capacity of DFS in the country’s response and recovery. In countries with only moderate DFS penetration, the benefits of DFS in improving aid response are unevenly distributed. While some populations, often urban or younger segments, may be able to access digital aid, others, particularly those in more remote areas, may be left out—causing disparities in recovery speed and effectiveness. In countries with low DFS penetration, aid delivery relies heavily on physical cash and in-person transactions, which can be delayed or disrupted by damaged infrastructure, increasing the risk of exclusion and slower recovery.

With 90 percent of adults with a formal financial account and 87 percent mobile money penetration, Kenya can capitalize on digital financial services to transfer emergency funds during climate disasters.³ Since 2013, the Kenyan Red Cross Society (KRCS) has leveraged mobile money to make cash transfers to Kenyan households affected by droughts, floods, and fires.⁴ Even in very remote parts of Kenya, mobile phones are widely accessible, enabling wide reach of humanitarian initiatives through mobile money. During the 2017 drought, KRCS created a recurring mobile phone-driven cash program, primarily using M-Pesa, that helped prevent nearly 250,000 people from slipping into severe food insecurity across 13 drought-ravaged counties.⁵ An evaluation of the program found that more than 60 percent of families in the program reported that they could afford three or more meals a day compared to 20 percent before the cash transfer initiative began.

Digital financial services also offer countries the opportunity to take pre-emptive action before a natural disaster strikes. In Bangladesh, which has frequently been impacted by flooding and cyclones, a significant portion of the population has a mobile money account, often on the bKash platform. In 2023, Bangladesh accounted for over 56 percent of mobile money accounts in South Asia.⁶ Preceding Cyclone Amphan in 2020, World Food Programme partnered with bKash to deliver anticipatory cash transfers through digital mobile money, enabling proactive engagement with affected communities before the peak of the disaster.⁷ bKash facilitated rapid aid distribution to over 23,000 vulnerable households, and recipients were 52 percent less likely to go a day without food during the flood.⁸ Three months later, households that received anticipatory aid through bKash accounts had higher earnings potential, reporting greater likelihood of avoiding crop loss or being able to replant as well as working for a wage, an early indicator of recovery.

In contrast, when Haiti experienced a severe earthquake in 2010, the country had very limited access to digital financial services. Most Haitians relied almost exclusively on cash for transactions, only 16 percent of the population had access to bank accounts, and digital financial services including mobile money were virtually nonexistent.⁹ With much of Port-au-Prince’s physical infrastructure—including banks, ATMs, and roads, damaged or destroyed—distributing cash aid was difficult and prolonged. Humanitarian organizations and the Haitian government had to physically transport large amounts of cash into affected areas, which exposed aid to theft, loss, and corruption.

Digital adoption decreases vulnerability

Digital payments have also proven to be a vital tool for maintaining economic activity during public health shocks. During the COVID-19 pandemic, digital payments emerged as a cornerstone of economic and business resilience, enabling firms and consumers to adapt rapidly to new constraints. As lockdowns and social distancing measures disrupted traditional, in-person transactions, businesses that could accept and process digital payments were able to maintain sales channels even when physical stores were closed.

Small businesses were disproportionately impacted by COVID-19.¹⁰ In comparison to larger firms, small businesses generally have fewer financial reserves, making them more vulnerable to sudden declines in revenue. According to a 2021 Visa Economic Empowerment Institute report, small businesses in the United States that adopted digital commerce and cross-border capabilities before and during the pandemic were significantly more resilient than those that did not.¹¹ Small businesses that were already selling online and equipped to accept e-commerce payments or that quickly pivoted to digital sales channels were able to maintain or even grow their customer base as consumer behavior shifted rapidly toward e-commerce during lockdown and social distancing measures. These businesses could continue serving existing customers and tap into new markets thanks to digital payment solutions and global e-commerce platforms.

Similarly, in the Middle East and Central Asia, digitally-enabled firms were able to mitigate economic losses arising from the pandemic better than digitally-constrained firms, with digitally-enabled firms facing a lower decline in sales by about four percent.¹² Digital readiness not only enabled businesses to weather the immediate impacts of the pandemic, but also positioned them for greater growth and resiliency in an increasingly digital and interconnected global economy.

COVID-19 also spurred an increased reliance on digital payments for consumers with digital financial accounts. During the pandemic, people needed a safe and contact-free way to make transactions in-person and a convenient way to make e-commerce transactions as many sales shifted online. In Latin America, approximately 20 percent of active Visa cards in the region made e-commerce transactions for the first time during the March 2020 quarter.¹³ And in April 2020, U.S. digital commerce—excluding the travel category—rose 18 percent.

Digital access enables stability

In the case of geopolitical crises, digital payments can provide stability for individuals and businesses navigating new uncertainties and upheaval. Throughout the Russia-Ukraine war, digital payments have helped to provide continuity and adaptability for Ukrainian residents amidst immense disruption. Beginning in February 2022, the National Bank of Ukraine (NBU) implemented several measures to maintain financial stability under martial law, including limits on cash withdrawals. In parallel, the NBU encouraged cashless payments and did not set any restrictions on domestic cashless transactions. The share of cashless card-based transactions rose to 68 percent of the total value of card-based transactions in Ukraine from May to December 2022, up from 60 percent over the same period in 2021.¹⁴ As millions of Ukrainians were forced to relocate, either within the country or abroad, digital payment systems allowed them to maintain access to their financial resources, support essential spending, and contribute to local economies where they resettled.

Other initiatives have also helped to facilitate the use and acceptance of digital payments around the country. In 2020, Ukraine launched Diia, meaning “action” in Ukrainian and an acronym for “the state and me,” which is a phone application and web portal that facilitates citizen-government interactions. Diia includes digital identification capabilities and accepts person-to-government payments from a variety of digital payment providers. The application also includes a virtual payment card, allowing Ukrainians to leverage government assistance and other funds using a single payment credential.¹⁵ Ukraine’s digital transformation led to 15.5 million Diia users, and by December 2023, Diia usage increased by 27 percent.¹⁶ Additionally, as the need for remote identification and verification of banking clients increased, NBU’s BankID system provided millions of Ukrainians with uninterrupted access to critical public and financial services, including digital versions of identification documents and the ability to remotely open accounts.¹⁷

In addition to facilitating secure transactions for those who remained close to the front lines, digital payments helped stabilize commerce in areas experiencing an influx of internally displaced persons. Card payment data shows that across all income groups, digital spending enabled displaced populations to quickly integrate into new local economies.¹⁸ The shift in purchasing power also provided a boost to businesses in the areas of Ukraine where many displaced people relocated.

Despite widespread displacement, consumer transactions and business activity—measured by card transaction data—stabilized through 2022, illustrating how digital payments facilitated ongoing economic activity even in a fragmented environment.¹⁹ While frontline areas saw over 60 percent loss among small businesses, other regions showed robust recovery. Central regions in Ukraine managed to recover 40 percent to 60 percent of economic activity, and in western regions, over 60 percent of businesses remained operational. Notably, the demand side—as measured by payment transaction data—has displayed even greater resilience than the supply side, suggesting strong consumer activity despite the challenges faced by businesses themselves.

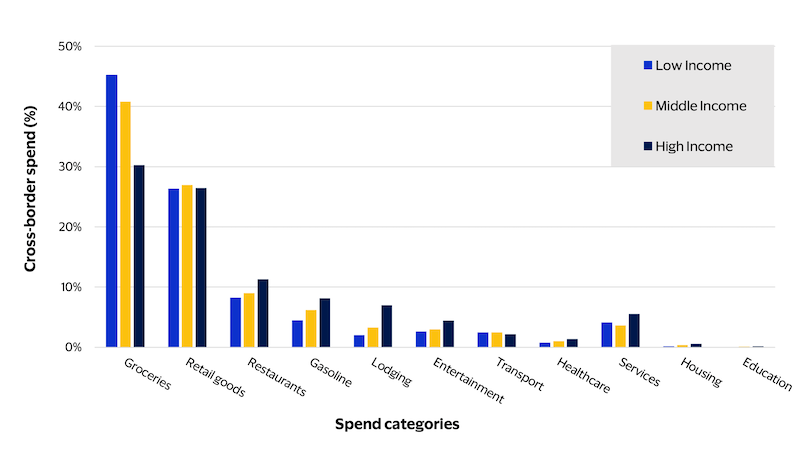

For Ukrainians who sought refuge abroad, digital payments were equally crucial. Transaction data indicates that in 2022, the percentage of active cardholders who made payments abroad nearly doubled.²⁰ The use of digital financial services allowed refugees to access their savings, pay for goods and services, and financially support themselves and their families while adjusting to new countries. Notably, lower-income consumers were more likely to migrate and draw on their savings abroad, and their spending was concentrated in essential categories such as groceries and retail goods.²¹ This not only supported individual resilience, but arguably generates economic spillovers to small businesses in host communities.

Cross-border spend by category on Ukraine-issued cards (2022)

Ukraine’s robust digital payments infrastructure was essential in maintaining economic links, facilitating aid distribution, and supporting recovery efforts during and after acute phases of the Russia-Ukraine war. Digital payment data demonstrated that non-discretionary merchants such as supermarkets were typically the first to recover, enabled by the persistent use of digital payments. Overall, the flexibility and reach of digital payment infrastructure proved indispensable in helping Ukraine weather the immediate shocks of war and lay the groundwork for eventual economic recovery and rebuilding.

Conclusion

Digital payments have emerged as a key factor of economic resilience and recovery during crises. Across the world, they have served as a vital lifeline for consumers and businesses, enabling economic activity to continue amid disruption. Critically, the level of maturity, sophistication, and adoption of digital infrastructure within a country significantly impacts how effectively a country can adapt to shocks, how successfully a country can maintain economic links, and how efficiently a country can facilitate the distribution of humanitarian aid.

Beyond access to digital infrastructure, people within a country should also have the necessary capabilities to properly leverage and utilize digital financial services to fully capitalize on their potential. Key pillars such as digital infrastructure, stable internet connectivity, banking development, financial inclusion, and financial literacy are all correlated with the prevalence of digital payments.

For governments and policymakers, this highlights the importance of investing in digital infrastructure, promoting digital and financial literacy, and adopting policies that encourage the use and acceptance of safe, secure, and reliable digital payments. Such measures will not only enhance economic resilience in the face of future crises but also ensure more inclusive and sustainable recovery if shock events increase in frequency and intensity around the world.

Footnotes:

- INFORM. (2024). INFORM Report 2024: Shared evidence for managing crises and disasters.

- Devex & Visa. (2024, May). Reimagining aid in the digital age: Building global capabilities to serve local needs.

- World Bank Group. (2025). The Global Findex Database 2025.

- Kenta Red Cross Society. (2019, May). Cash Preparedness Case Study.

- Red Cross Red Crescent Climate Centre. (2017, July 12). Kenya Red Cross steps up humanitarian relief as drought fails to relinquish grip.

- GSMA. (2024). The State of the Industry Report on Mobile Money 2024.

- Vidal, J. J. (n.d.). Case Study: Anticipatory Action and Mobile Money, Bangladesh. IE Insights..

- Pople, A., & Dercon, S. (2024, July 25). Cash Before Calamity: Anticipatory Action for Flood Resilience. Center for Global Development.

- Evidencity. (2023, September 15). Haiti’s financial Inclusion Journey; Taylor, E. B., Baptiste, E., & Horst, H. A. (2011, April). Mobile Money in Haiti: Potentials and Challenges. Institute for Money, Technology and Financial Inclusion.

- Kang, W., & Wang, Q. (2022, October 17). The Impact of COVID-19 on Small Businesses in the US: A Longitudinal Study from a Regional Perspective. International Regional Science Review 46(3).

- Kotschwar, B. (2021, October). Helping the hardest hit: Recovery and resilience for small business in the United States. Visa Economic Empowerment Institute.

- Abidi, N., El Herradi, M., & Sakha S. (2023, May 4). Digitalization and resilience during the COVID-19 pandemic. Telecommunications Policy 47(4).

- Bary, M. (2020, May 18). Visa sees ‘massive’ digital acceleration with millions trying e-commerce for the first time. Market Watch.

- National Bank of Ukraine. (2022). Power Banking: Annual Report 2022.

- United Nations Development Programme. (2025, August 18). New Diia.Card consolidates government payments into a single account.

- Ingram, G., & Vora, P. (2024, January 30). Ukraine: Digital resilience in a time of war. Brookings.

- Poddyerogin, A. (2023, July 28). Payments in wartime: the story of the National Bank of Ukraine. European Payments Council.

- Based on author’s analysis of Visa data.

- Based on author’s analysis of Visa data.

- Based on author’s analysis of Visa data.

- Cardholder income imputed based on total card purchase volume in 2021, with top quartile of cards within the city of residence classified as high-income.