The supply of fiat-backed stablecoins—digital assets issued on blockchain networks and designed to maintain a stable value relative to a specific currency (e.g. U.S. dollar)—continues to soar, reaching approximately $238 billion in August 2025, according to Visa Onchain Analytics data. With stablecoin supply now more than 60 times higher than its value at the beginning of 2020, it’s no wonder policymakers around the world are moving quickly to establish comprehensive regulatory frameworks to address issues like financial stability, consumer protection, and systemic resilience. Policymakers have now provided additional clarity on what they expect from stablecoin issuers and how they plan to regulate these assets. This report examines the potential implications that recently enacted stablecoin reserve asset regulation could have on the business models of stablecoin issuers, and how these regulations might impact the future of payments.

Recently enacted stablecoin legislation

An examination of recently enacted stablecoin legislation in four key jurisdictions—the United States, European Union, United Arab Emirates, and Hong Kong—highlights considerable similarities in reserve asset requirements, as discussed/mentioned in the following section. For example, all jurisdictions require stablecoin providers to back their stablecoin issuance on at least a 1:1 basis with high quality liquid assets (HQLA). Furthermore, it’s also standard that reserve assets must be denominated in the same currency as the stablecoin reference peg and the payment of interest by issuers to stablecoin holders is prohibited.

Reserve asset requirements for recently enacted stablecoin legislation

Reserve asset requirements

- Issuance must be backed on a 1:1 basis with high-quality liquid assets (HQLA)

- Assets must be denominated in the same currency as the reference peg

- Payment of interest by issuer to stablecoin holder is prohibited

United States: GENIUS Act

Allowable assets:

- Cash

- Bank deposits

- U.S. Treasuries

- Overnight (reverse) repurchase agreements

- Investment Funds

Asset Maturity Duration:

≤ 93 days

European Union: Markets in Crypto Assets

Allowable assets:

- Minimum 30% in bank deposits

- 60% if issuer is significant¹

- Remaining in HQLA with minimal risk

- 35% limit on assets from single entity

Asset Maturity Duration:

n/a

United Arab Emirates: Payment Token Services

Allowable assets:

- Non-bank entity

- Entire reserves held in cash

- Bank-owned subsidiary

- At least 50% in cash

- UAE gov’t/central bank securities

Asset Maturity Duration:

≤ 6 months

Hong Kong: Stablecoins Bill

Allowable assets:

- Cash

- Bank deposits

- Marketable debt

- Overnight (reverse) repurchase agreements

- Investment funds

Asset Maturity Duration:

≤ 1 year

A central pillar of these frameworks is the requirement that stablecoin issuers maintain adequate reserves to back their digital liabilities. Although the specific composition of reserves varies across jurisdictions, stablecoin reserve assets typically include substantial holdings of government securities—either directly or indirectly through overnight reverse repurchase agreements²—as well as commercial bank deposits.

Regulatory influences on stablecoin business models

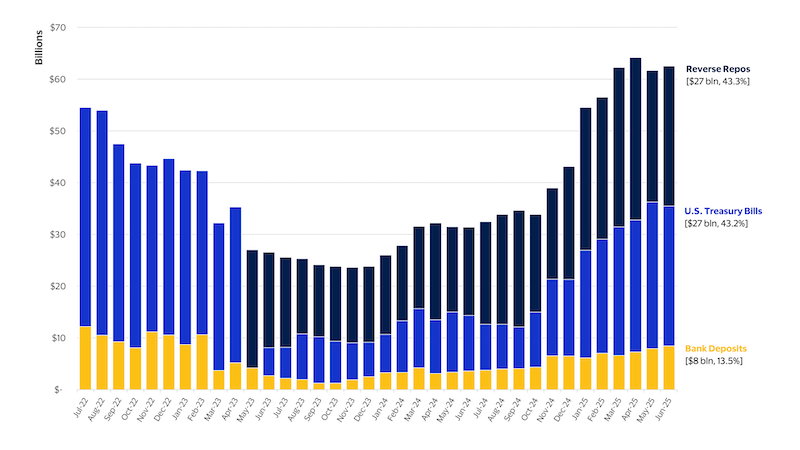

Requiring stablecoin issuers to hold high-quality liquid assets, including government debt securities and bank deposits, is likely to have little impact in the short-term, as many stablecoin issuers already back their stablecoins with these assets. For example, data on USDC, the U.S. dollar-pegged stablecoin issued by Circle Internet Group, Inc. (“Circle”) and currently the second largest stablecoin by market capitalization, illustrates that reserves have been comprised almost exclusively of U.S. Treasury bills, reverse repos, and bank deposits (see Figure 1 below), since at least July 2022.³

Figure 1: Reserve holdings for USDC stablecoin

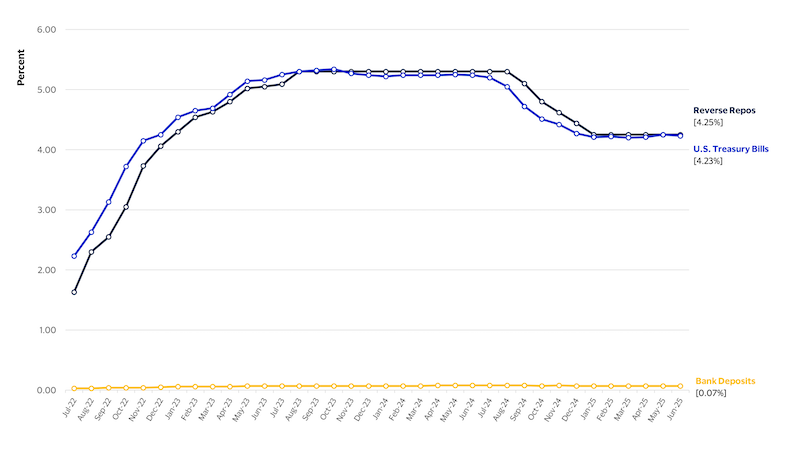

The logic for this arrangement is straight forward: by holding bank deposits and government securities—high-quality, risk free assets that can be liquidated quickly to meet redemption needs—stablecoin issuers hope to convey to consumers (and the market) that these new digital assets are safe and secure. Additionally, the yield earned from holding these assets provides an important revenue source. A look at historical interest rates on applicable stablecoin reserve assets in the U.S. (see Figure 2 below) provides helpful context for the current asset allocation of USDC reserves.

Interest rates on reverse repos and U.S. Treasury bills have been significantly higher than those associated with bank deposits for the past several years, which is reflected in the substantial allocation of USDC reserves to reverse repos (43.3 percent) and U.S. Treasury bills (43.2 percent), as compared to bank deposits (13.5 percent), which is highlighted in Figure 1 above.

Figure 2: Average interest rates on acceptable stablecoin reserve assets in the U.S.

Stablecoin issuers may face considerable interest rate and counterparty risk

Although this strategy provides a sense of stability for stablecoin holders, it also makes stablecoin issuers highly dependent on returns generated from holding government securities and exposes them to potential counterparty risk. There is no better example of the interest rate and counterparty risks faced by stablecoin issuers than that of Circle and its USDC stablecoin.

From 2022 to 2024, the income Circle received from the interest earned on the assets held in its USDC reserves accounted for 95 to 99 percent of total revenue, according to the company’s S-1 filing. Given this significant exposure to interest rate risk, Circle analyzed the potential impact that hypothetical changes in interest rates would have on their reserve income. Assuming USDC in circulation and reserve asset allocations were held constant at end-2024 levels, a reduction in interest rates from an average yield of 4.33 percent (in December 2024) by 100 basis points is estimated to reduce reserve income by $441 million for the year ending December 2025, an amount equal to approximately one-quarter of total revenue in 2024.

With respect to counterparty risk, Circle’s exposure to Silicon Valley Bank (SVB) proved considerable. In the midst of SVB’s collapse in March 2023, Circle revealed—through a tweet—that $3.3 billion of its approximately $40 billion in USDC reserves was effectively trapped with the struggling bank. The news prompted fears that Circle may not have enough available collateral to meet redemptions and ultimately resulted in USDC breaking its 1:1 peg, trading as low as 87 cents on the secondary market.⁴ Two months later, in May 2023, USDC reserves were hit by another (though less severe) counterparty shock when the looming debt crisis in the U.S. caused Circle to cut its exposure to short-term U.S. Treasuries amid concerns about the U.S. government’s ability to pay its debts, according to a Bloomberg article. As highlighted in Figure 1 above, U.S. Treasury bill exposure in USDC reserves was entirely replaced in May 2023 by reverse repo contracts, which became a significant part of its reserve allocation mix even after U.S. Treasuries were re-introduced.

Revenue on reserve assets likely to be buffeted by expected decline in rates

The passage of the GENIUS Act in the United States should not materially impact the business operations of stablecoin issuers in the short-term, as noted earlier, since the assets they currently invest in are among the acceptable reserve assets, e.g. cash, bank deposits, U.S. Treasuries (with remaining maturities of 93 days or less), and repurchase agreements (including reverse repos). Furthermore, U.S. regulations do not prescribe allocation amounts or limits on these assets, allowing stablecoin issuers to optimize the asset allocation mix as they see fit.

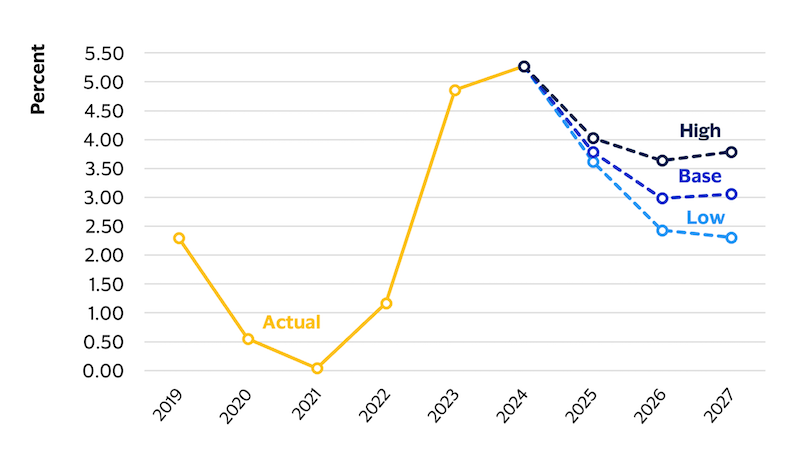

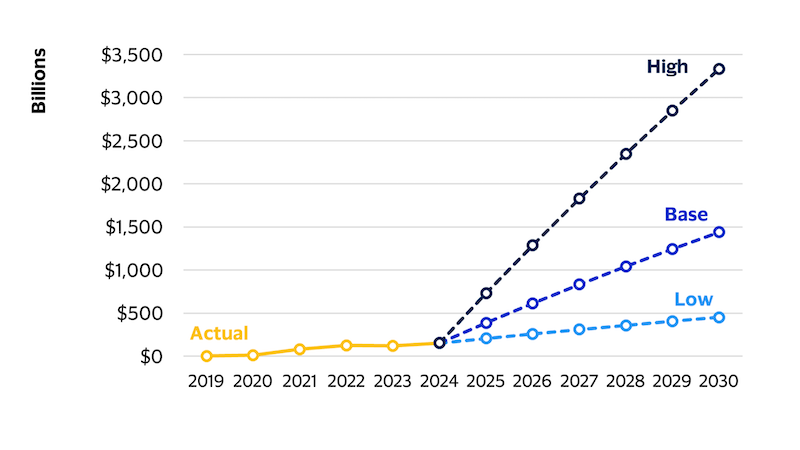

However, these regulations will not alleviate interest rate and/or counterparty risks faced by stablecoin issuers. With U.S. interest rates expected to decline over the next few years (see Figure 3 below), stablecoin issuers can likely expect a corresponding reduction in reserve asset income. Of course, this decline may be offset by an increase in stablecoin supply. Given the recent passage of stablecoin legislation, many market participants are quite optimistic about future stablecoin growth. For example, Citi Institute released a report in April 2025 suggesting that by 2030, total stablecoin issuance could climb to as high as $3.7 trillion—though the base case is for a $1.6 trillion increase, with a lower bound estimate at $500 billion (see Figure 4 below).5 6

Figure 3: Forecasts of U.S. interest rates

Figure 4: Forecasts of USD stablecoin supply growth

To understand how a potential decline in U.S. interest rates, coupled with an expected rise in stablecoin supply, may ultimately impact revenue projections for GENIUS Act compliant stablecoin issuers of U.S. dollar-denominated stablecoins, the following assumptions are made:

- Stablecoin issuers of U.S. dollar-denominated stablecoins will maintain a reserve asset allocation mix identical to that of the USDC reserve (e.g. 85 percent in U.S. Treasuries, and 15 percent in bank deposits).

- U.S. dollar-denominated stablecoin supply increases to $1.4 trillion by 2030, as projected by Citi Institute’s base case.

- U.S. interest rates decline by approximately 200 basis points by 2027, before stabilizing, as projected using monthly forecasts of the Secured Overnight Funding Rate (SOFR) available at EconForecasting.⁷

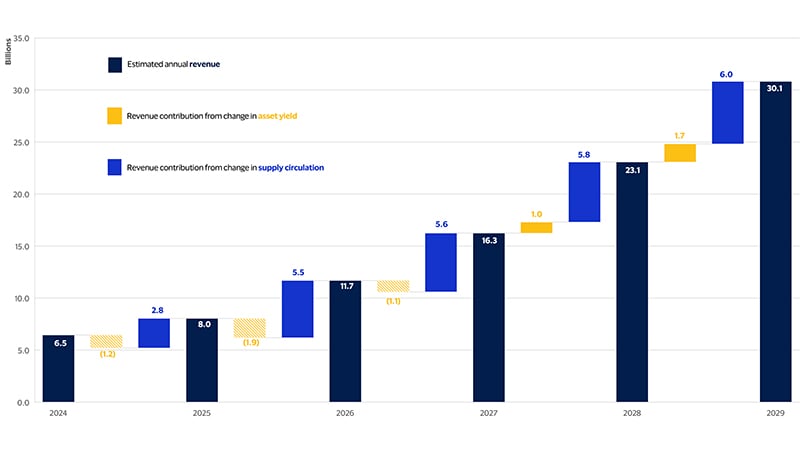

Assuming these assumptions are correct, it’s likely that the positive impact from the increase in stablecoin supply will outweigh the negative effects from declining interest rates, ultimately resulting in a modest increase in annual revenues (see Figure 5 below). For example, annual revenues between 2025 and 2027 could rise by about $8 billion, supported by approximately $11 billion in contributions from rising stablecoin supply, offsetting the potential $3 billion decline in revenue from the expected drop in interest rates.

Figure 5: Estimated annual revenue from U.S. dollar-pegged stablecoin reserve assets

Should interest rates decline more than expected, or supply forecasts prove to be overly optimistic, stablecoin issuers will need to consider alternative revenue sources. Indeed, Circle has already noted they are looking at ways “to monetize the activity on our network with products that earn fee-based revenues based on transactions and usage in the future”. The recent announcement of the Circle Payments Network appears to be a step in that direction.

Of course, revenues are only one side of the equation. Complying with new stablecoin regulations requiring certification of anti-money laundering (AML) and know your customer (KYC) programs may incur additional (and recurring) costs that stablecoin issuers have not had to fully consider yet. If these costs become considerable, and new sources of revenue do not outweigh these costs, stablecoin issuers may find their current business models prove untenable.

Prescriptive regulatory environment in Europe, UAE may hinder stablecoin growth

Europe provides a helpful example of the limitations of the current stablecoin business model. From 2015 to 2022, negative interest rates persisted in Europe, making it economically infeasible to issue a euro-pegged stablecoin during that period. Although euro-pegged stablecoins now represent the largest non-U.S. dollar denominated stablecoins, with a market capitalization of $410 million, they account for just 0.16 percent of total issuance, according to data from DeFiLlama.

Going forward, the reserve asset requirements enshrined in the European Union’s Markets in Crypto Assets (MiCA) regulation could impair the ability of stablecoin issuers to maximize revenue from interest earned on assets, thus potentially hindering the growth of stablecoins in the region. Unlike the GENIUS Act, which does not prescribe specific allocation levels for stablecoin reserve assets, MiCA requires that stablecoin issuers must hold a minimum of 30 percent of total reserves in bank deposits—and that figure doubles to 60 percent if the issuance amount grows to be “significant”.⁸

To better understand the impact MiCA could have on a stablecoin issuer, let’s compare the expected annual revenue for a (non-significant) stablecoin with €4.9 billion in issuance to one with €5.0 billion, which would thus be considered significant as defined by the regulation. Assuming an average overnight deposit interest rate of 0.51 percent and a yield of 1.99 percent for a 3-month government bill,⁹ the non-significant stablecoin issuer could expect to earn approximately €75.8 million on its €4.9 billion reserve. If issuance increased to €5 billion from €4.9 billion, that same issuer could see annual revenues fall by about 27 percent to €55.1 million, due to its “significant” status and the necessary change in reserve allocations that would be required.¹⁰

In Hong Kong and the United Arab Emirates, there is currently no meaningful stablecoin issuance denominated in local currency. Should stablecoin supply in these countries increase materially, stablecoin issuers in Hong Kong will be able to invest in any asset that is “of high quality and high liquidity with minimal investment risks” with no prescribed allocation levels, according to recently enacted legislation.¹¹ Meanwhile, reserve asset requirements in the United Arab Emirates are even more restrictive than those in the EU. Under the UAE’s Payment Token Services Regulations, stablecoin issuers that are wholly owned subsidiaries of a bank must hold 50 percent of reserves as cash in a segregated escrow account and may invest the remaining 50 percent in UAE government bonds and monetary bills from the Central Bank of the UAE. For issuers not owned by a bank, 100 percent of the reserves must be held as cash in an escrow account.

Conclusion

The global regulatory landscape for stablecoins is rapidly evolving, reflecting both the exponential growth of these digital assets and the urgency among policymakers to safeguard financial stability. As highlighted throughout this analysis, jurisdictions such as the United States, European Union, United Arab Emirates, and Hong Kong are converging on a set of core regulatory principles—most notably, the requirement for 1:1 reserve backing with high-quality liquid assets (HQLA), currency-matching of reserves, and prohibitions on interest payments to stablecoin holders. These standards aim to mitigate systemic risk, enhance consumer protection, and ensure the resilience of payment systems.

However, the impact of these regulations extends far beyond compliance. For stablecoin issuers, the shift toward stringent reserve requirements and operational transparency may necessitate adjustments to business models, particularly in how revenue is generated, and risks are managed. Additionally, these regulations are likely to have broader implications for global financial markets. The potential ripple effects of stablecoin legislation on the balance sheets of commercial banks, as well as the demand for government securities, will be explored in a forthcoming report by the Visa Economic Empowerment Institute.

Ultimately, the trajectory of stablecoin regulation will shape the future of digital finance. A well-calibrated regulatory framework can foster innovation while preserving trust and stability. Conversely, overly rigid or fragmented approaches risk stifling progress and creating regulatory arbitrage. As such, continued dialogue between regulators, industry participants, and policymakers will be essential to strike the right balance. The path forward must be guided by principles that are risk-sensitive, technology-neutral, and globally interoperable—ensuring that stablecoins can fulfill their promise as a secure, efficient, and inclusive component of the modern financial ecosystem.

Footnotes:

- Criteria for “significant” stablecoins for MiCA include 1) more than 10 million stablecoin holders, 2) a market capitalization greater than €5 billion, and 3) an average number and aggregate value of daily transactions exceeding 2.5 million transactions and €500 million, respectively.

- In a reverse repurchase agreement (reverse repo) the stablecoin issuer effectively lends cash to another party in exchange for collateral (typically government bonds). At the end of the term (usually overnight), the other party pays back the cash, plus interest, to the stablecoin issuer and receives its collateral in return.

- Prior to July 2022, the monthly reserve account reports for data on USDC, provided by Circle, list only the “total fair value of U.S. dollar denominated assets held on behalf of USDC holders” and do not divulge the specific assets held in reserve.

- Research by the Digital Currency Initiative at MIT suggests that while the USDC peg broke for retail users on the secondary market, it held up for institutional clients with primary market access.

- It should be noted that the Citi Institute report expects the percentage of U.S. dollar denominated stablecoins to decline to 90 percent of the total by 2030, from 99.8 percent currently. This would suggest estimates for total U.S. dollar denominated stablecoin supply by 2030 would range from $450 billion (Low) to $3.3 trillion (High), with a Base case of $1.4 trillion.

- Following the drafting of this paper, the Citi Institute updated its forecast for stablecoin issuance by 2030, increasing its base case to $1.9 trillion, while also shifting its High and Low estimates to $4 trillion and $900 billion, respectively. Nonetheless, the analysis presented in this report will continue to be based on the April 2025 estimates.

- Forecasts are calculated as of September 2, 2025. The use of SOFR mirrors the calculation method provided by Circle regarding its USDC reserve, in which it notes that income on reserve assets is earned “historically at rates at a discount to the prevailing SOFR during the applicable periods”. Analysis of the reserve return rate compared to the quarterly average SOFR, both provided in Circle’s S-1 filing, suggests the “discount” noted above is approximately 16 basis points. This discount is used in the author’s calculations.

- Criteria for “significant” stablecoins for MiCA, include 1) more than 10 million stablecoin holders, 2) a market capitalization greater than €5 billion, and 3) an average number and aggregate value of daily transactions exceeding 2.5 million transactions and €500 million, respectively.

- Deposit rate according to data from the European Central Bank, 3-month government bill rate according to data from the Federal Reserve Bank of St. Louis. Both rates as of July 2025.

- Of note, if MiCA did not prescribe specific allocation levels at all and the stablecoin issuer were allowed to invest its €5 billion reserve similar to USDC under the GENIUS Act in the U.S., the annual revenue generated would be approximately €88.4 million.

- Guidance from the Hong Kong Monetary authority provides more clarity on the composition of these assets, including cash, bank deposits, marketable debt securities, reverse repurchase agreements, and investment funds.