Visa Perspectives

Payments insights from around the globe, designed to help you navigate the new world of commerce

-

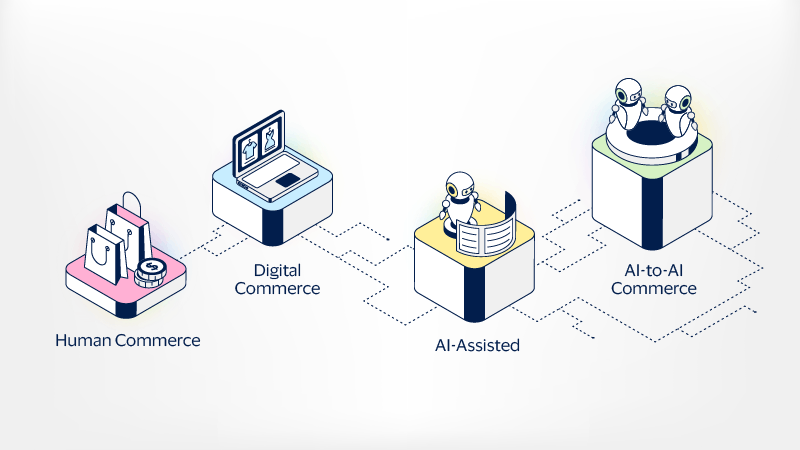

Agentic Commerce: The expanded payments economy

The next era of commerce

When AI becomes the customer

Spotlight

Quick access to trending stories, the latest research, and breaking news updates

Today’s Playlist

Recent picks from Visa’s YouTube channel featuring stories about modern commerce in video format.

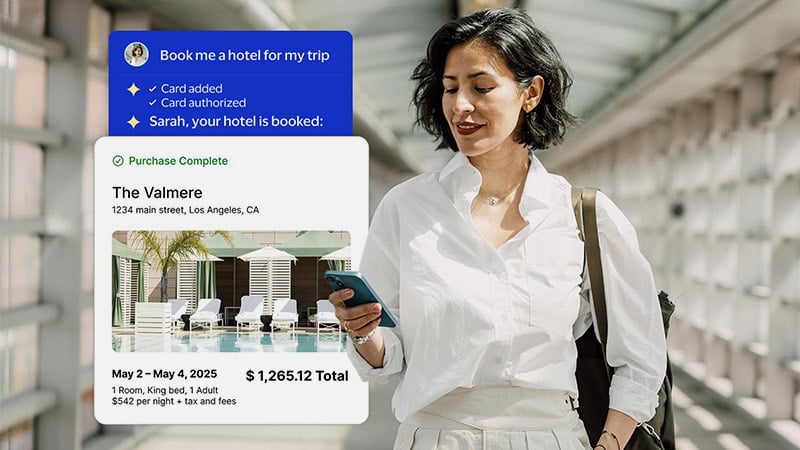

Find and buy with AI

Introducing Visa Intelligent Commerce

How AI agents will shop for you

Visa Intelligent Commerce explained

Visa & Main

A platform built to champion small businesses at the corner of commerce and community