Visa Perspectives

Payments insights from around the globe, designed to help you navigate the new world of commerce

-

Visa Releases Its AI-Powered Cyber Defense System to Open Source

Our participation in Anthropic’s Project Glasswing reflects a proactive approach to testing advanced AI for cybersecurity and strengthening the global payments ecosystem.

Visa shares vision for intelligent, programmable commerce

From AI-driven transactions to stablecoin settlement and next-gen tokens, Visa is redefining the trust and connectivity layer powering global commerce

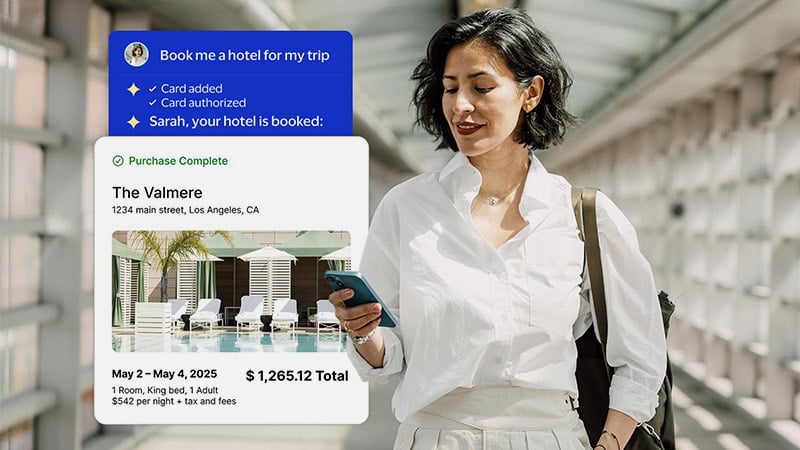

How Visa and OpenAI Are Building the Future of AI Commerce

Consumers are increasingly turning to AI agents to help them shop, compare, and buy. Visa and OpenAI are partnering to build infrastructure designed to make AI commerce secure, scalable, and seamless.

Spotlight

Quick access to trending stories, the latest research, and breaking news updates

Today’s Playlist

Recent picks from Visa’s YouTube channel featuring stories about modern commerce in video format.

Find and buy with AI

Introducing Visa Intelligent Commerce

How AI agents will shop for you

Visa Intelligent Commerce explained

Visa & Main

A platform built to champion small businesses at the corner of commerce and community