Then comes the awkward pause

Both parties have agreed on price, volume and delivery timelines. But now there’s payment timing to consider alongside cross border transfer and banking cut-off hours. It’s already Saturday morning in Asia. The supplier wants to know if they can receive payment by Monday morning their time. While the deal is solid the payment rails aren’t moving at the same speed.

Enter stablecoin payments: What they are (and what they’re not)

This is where stablecoin payments may enter the conversation. Stablecoins are often misunderstood but increasingly relevant. In plain terms, stablecoins are blockchain-based digital assets that are pegged one-to-one to fiat currencies, such as the U.S. dollar or the Euro. Their purpose isn’t speculation but reliability.

For B2B payments, that distinction matters. Stablecoins can potentially offer value stability that businesses can trust, availability that extends beyond traditional banking hours and programmability that supports modern, automated workflows. They can also be transferred across borders, making them well suited to global commerce. The simplest way to think about them is as digital cash for the internet age.

Visa now has expanded optionality on payment endpoints and settlement efficiency on the Visa Direct network to include stablecoins:¹

-

-

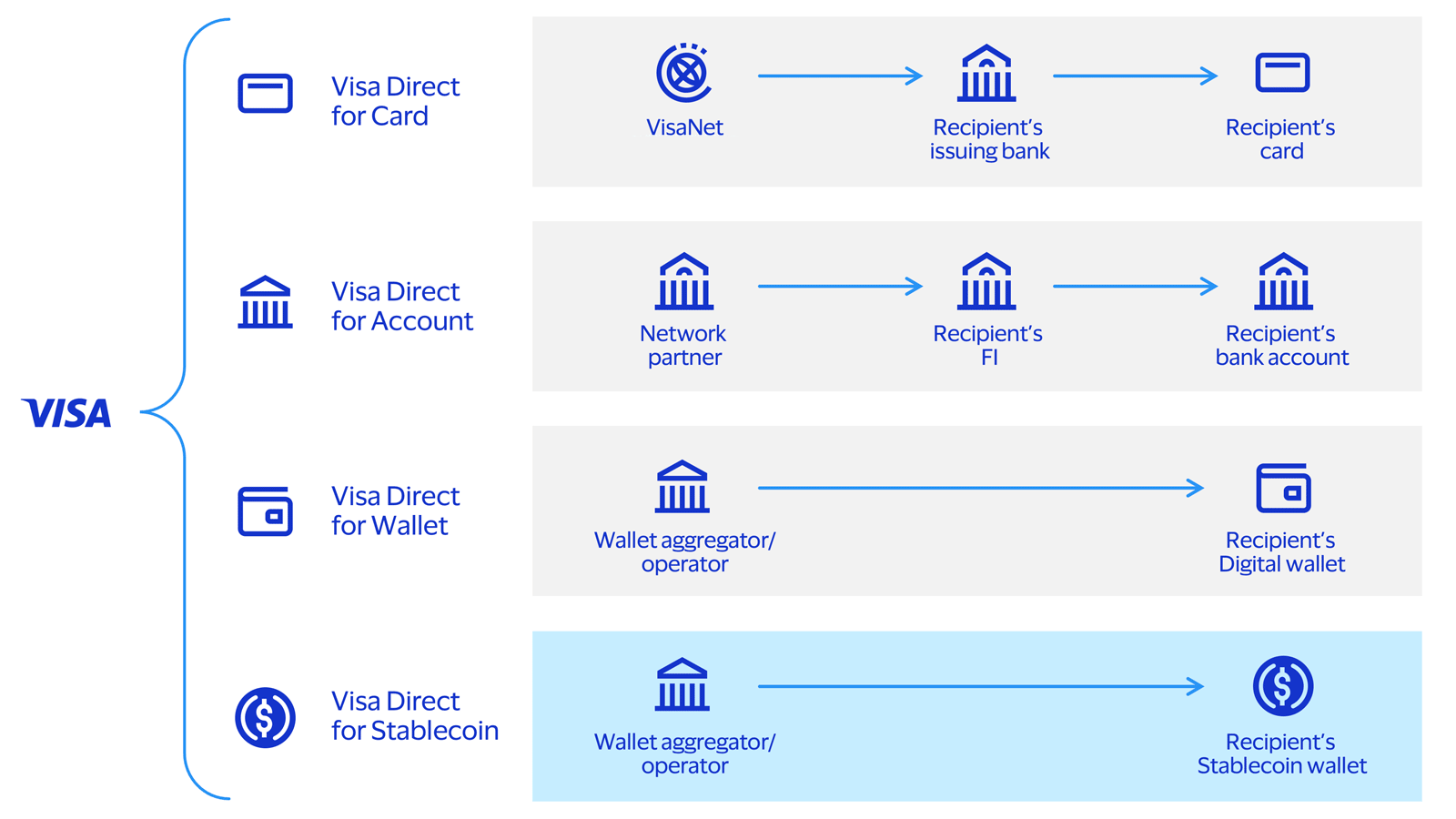

Visa Direct clients have previously had three options for payment endpoints:

- Visa Direct for Card – VisaNet transfers funds to the recipient's issuing bank, and they transfer the funds to the the recipient's card.

- Visa Direct for Account – A network partner transfers funds to the recipient's financial institution, and they transfer the funds to the recipient's bank account.

- Visa Direct for Wallet – A wallet aggregator or operator transfers funds to the recipient's digital wallet.

Now there is a fourth option, based around stablecoin: - Visa Direct for Stablecoin – A wallet aggregator or operator transfers funds to the recipient's stablecoin wallet.

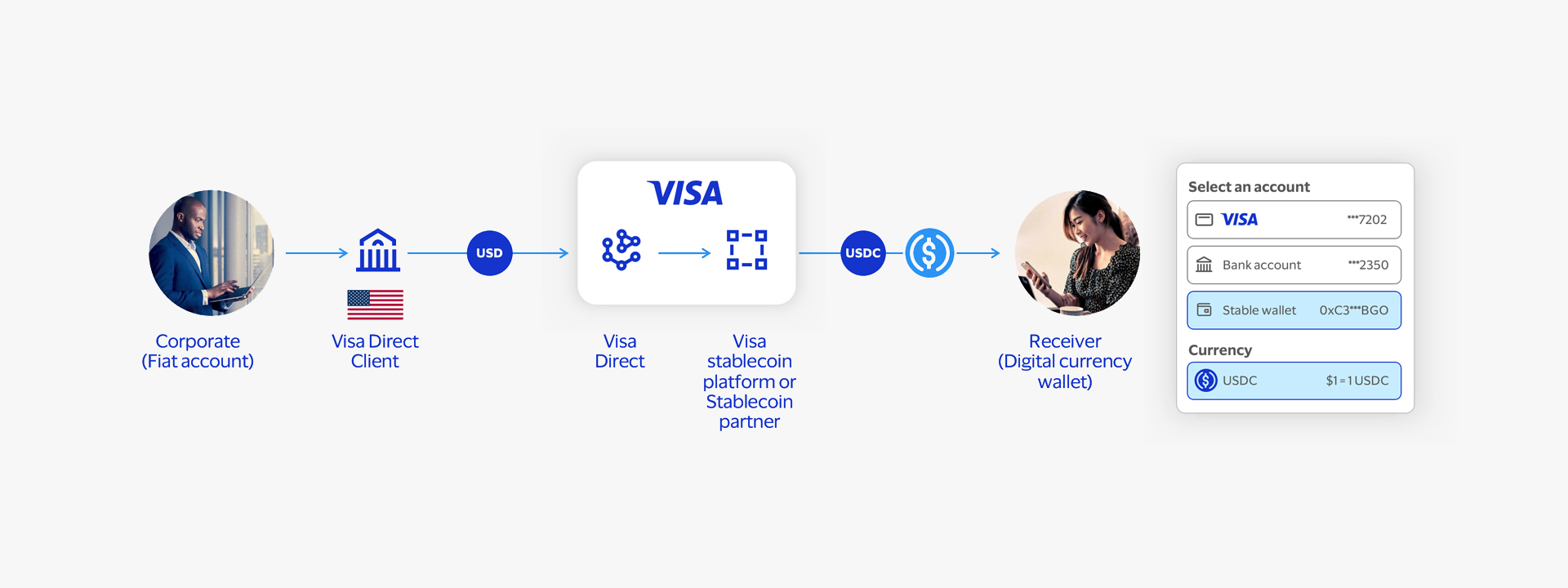

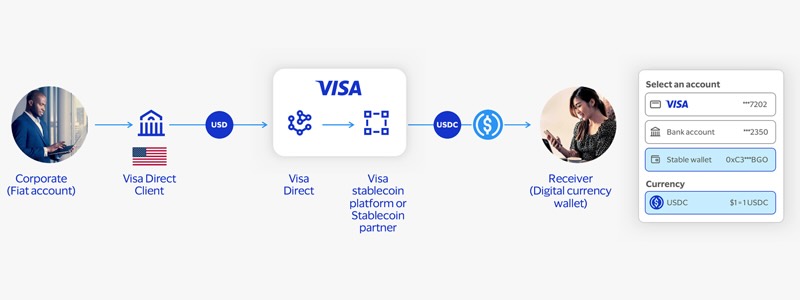

Stablecoins offer new currency options for payouts

Now, with stablecoins, Visa Direct clients can prefund their account in fiat while eligible senders can payout to a stablecoin wallet - providing enhanced reach, expanded currency options and greater flexibility.¹

Image shows B2C and B2B use cases where the recipient elects to receive stablecoins.

-

-

A cross-border B2B or B2C payment is described. The corporate client, operating a fiat account, instructs their U.S. bank to their recipient. The payment leaves the client in USD, and within the Visa Direct ecosystem, working with a stablecoin platform or partner, the payment is executed in USDC stablecoin. The recipient operates a banking facility that enables receipt of USDC stablecoins into a digital wallet.

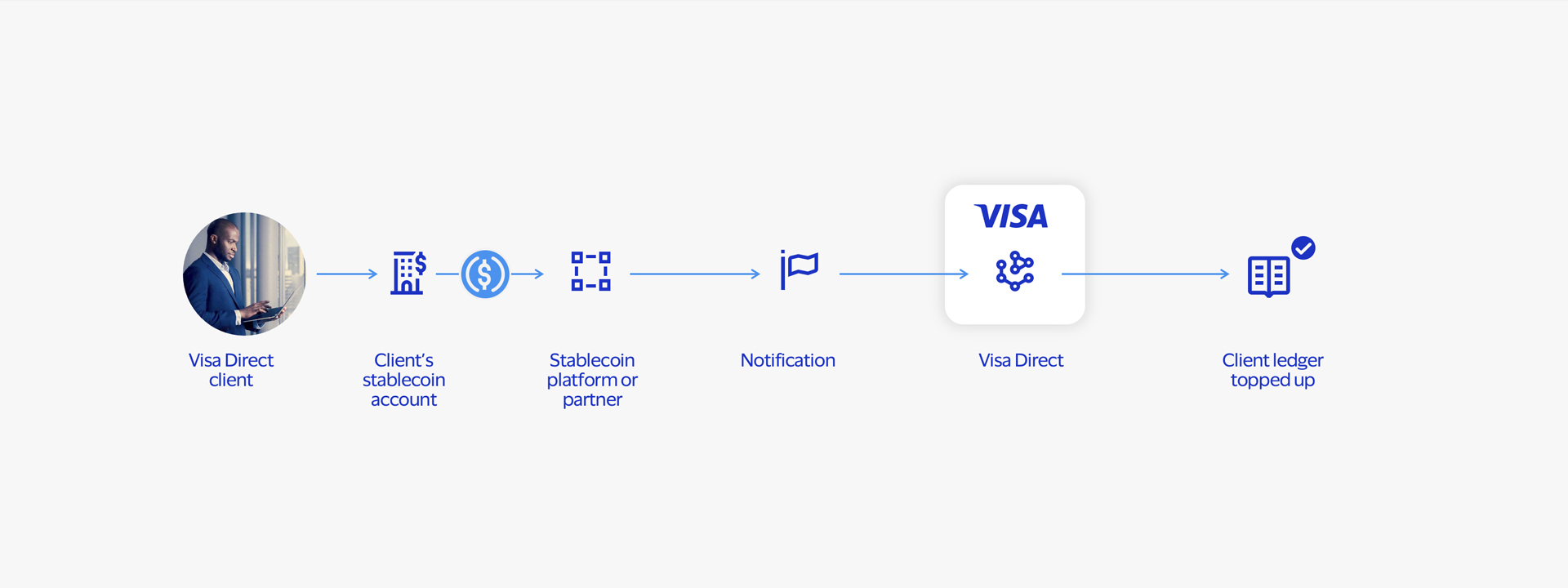

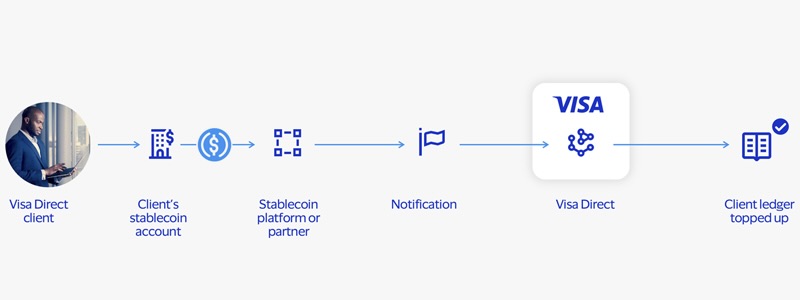

Around-the-clock prefunding with stablecoins

Image shows a scenario where the client either holds stablecoins already, or requires faster prefunding options.

-

-

The image depicts how stablecoin prefunding works. A Visa Direct client has a stablecoin account. Stablecoin funds are transferred with assistance from a stablecoin platform, via Visa Direct to the client’s ledger. A notification is issued as the transaction happens.

The features that distinguish B2B stablecoin payments

Stablecoin settlement can help make B2B payment acceptance more practical by tackling some of the cash‑flow constraints that have long held suppliers back. Wire, for example, can be slow and unpredictable in terms of timeline and cost. Concerns like slow settlement, pressure on working capital and added operational complexity can eat into already thin margins. Stablecoins, meanwhile, work as a complement to existing payment strategies.

By pairing card acceptance with stablecoin settlement, new opportunities arise. Shorter settlement and FX windows within cross-border transactions can help increase access to liquid funds and reduce reliance on short‑term financing, allowing suppliers to access funds sooner and manage cashflow more effectively. This can provide benefits for reconciliation and working capital management. Together, B2B card acceptance and stablecoin settlement support a payment model that can scale efficiently and works well for both sides of the transaction.

These dynamics matter most in cross‑border B2B payments. Delays can strain supplier relationships and tie up liquidity longer than necessary through prefunding and collateral requirements. In many emerging markets, access to major currencies can be limited or expensive, leaving suppliers exposed to currency volatility that can directly impact margins.

Stablecoin cross-border payments can help reduce these frictions by enabling prompt settlement across geographies. Funds can move outside traditional banking hours, including weekends, with fewer intermediaries involved. This can help improve cash‑flow predictability for both buyers and suppliers. Stablecoins can also give businesses greater flexibility over when and how they convert into local or major currencies, reducing FX friction. All of this can happen within existing card authorization and acceptance flows. The transaction experience stays the same for cardholders, while stablecoin settlement can be fast, simple and efficient once approval is complete.

Why now? Enter agentic AI

With the emergence of agentic commerce, and as more businesses operate directly in stablecoins, we can expect that they will increasingly rely on agents acting on their behalf to conduct commerce. These agents are expected to be able to negotiate terms, agree on pricing, manage timing and coordinate settlement directly with counterpart systems. For this kind of agent‑to‑agent (A2A) commerce to work, value needs to move in a form that is always available, predictable, and suited to automated execution, which is why stablecoins become essential.

At the same time, these agents must operate within clear limits and controls, with defined authorization, spending thresholds and visibility. Once terms are agreed, businesses still need practical ways to execute payment through existing acceptance. Stablecoin‑linked commercial cards allow automated agents to pay via standard card rails while funding transactions from always‑available, programmable stablecoin balances.

See our agentic commerce series for more information. More about Visa and AI

Stablecoin payments in action: From agreement to settlement

Returning to the opening scenario, the end-to-end flow between the North American buyer and the Chinese supplier becomes far more elegant with the stablecoin option. The two companies can negotiate terms digitally and finalize the agreement within predefined parameters. Once those parameters are met, the payment obligation is automatically triggered. Settlement then occurs using a stablecoin, reducing delays and giving the supplier faster access to funds.¹

Of course, ensuring these solutions are implemented with privacy and data confidentiality is critical. Sensitive negotiations often stay off-chain. While countries are increasingly opening their arms to stablecoin use cases, regulatory requirements vary by region. Cost predictability is also important, and corporations expect fixed fees rather than surprises. Stablecoin payments are powerful, but corporate-grade execution is what makes them practical.

This is where issuers and fintechs have a clear opportunity. Issuers can enable stablecoin settlement options that complement existing payment products. Fintechs can build wallets, on- and off-ramps and program management layers that integrate seamlessly into current workflows. Together, they can unlock new revenue models, deliver better client experiences and differentiate meaningfully in cross-border B2B payments. Collaboration across the ecosystem is not optional; it is essential.

The bigger picture: Borderless money that actually works

Viewed more broadly, stablecoin payments represent a bridge between traditional finance and digital-native commerce. They make it possible for money to move at the speed of business, supporting always-on commerce at global scale. Stability, it turns out, can be pretty disruptive.

So, we return once more to that Friday afternoon deal. The agreement is the same, the counterparties are the same, but the outcome is different. Settlement happens smoothly, without waiting for Monday morning. Stablecoins are no longer experimental concepts; they are becoming operational tools. The future of commercial payments isn’t about reinventing the system. It’s about making it work better, every day of the week.

ABOUT THE AUTHOR

Mark Nelsen

Head of Product, Commercial & Money Movement Solutions, Visa

Mark oversees product development that helps people, businesses, and governments move money quickly and safely. He leads global product strategy for commercial credentials, digital money movement, and secure B2B payments. He has been with Visa for more than 20 years.

Visit our AI knowledge hub

How and where Visa is working to bring agentic AI into the world of commerce and payments.