Visa Perspectives

-

Visa Releases Its AI-Powered Cyber Defense System to Open Source

Our participation in Anthropic’s Project Glasswing reflects a proactive approach to testing advanced AI for cybersecurity and strengthening the global payments ecosystem.

Rethinking the great wealth transfer: What the data really shows

Visa’s U.S. Economist Sean Windle explains why the great wealth transfer may be smaller than headline estimates suggest and why its impact is already visible in housing, travel and other major financial decisions

AI and digital commerce drive resilience in today’s economy

Richard Lung, Principal Global Economist at Visa Business and Economic Insights, discusses the economic outlook, consumer adaptation, digital commerce trends and the role of AI investment in growth.

Spotlight

Quick access to trending stories, the latest research, and breaking news updates

Today’s Playlist

Recent picks from Visa’s YouTube channel featuring stories about modern commerce in video format.

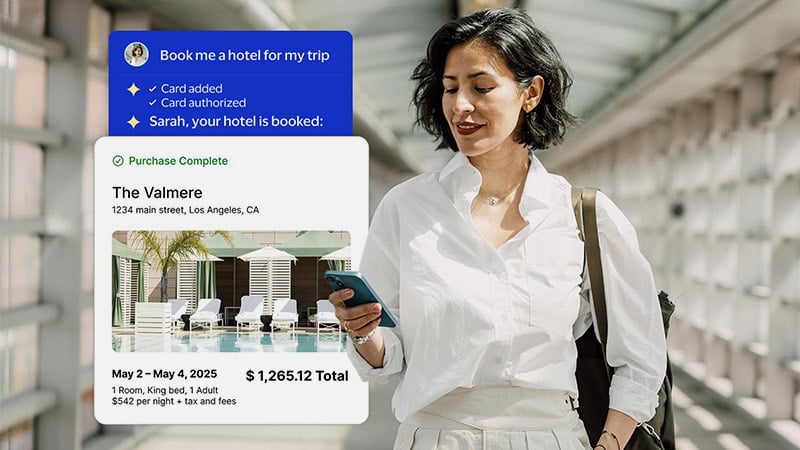

Find and buy with AI

How AI agents will shop for you